A better way to value companies

Want to use this calculator for yourself?

As the saying goes: “all models are wrong, but some are useful.”

Over the years, we’ve used many valuation multiples — P/B, P/E, and P/S — that sometimes stop being useful, as market environments change.

In the last ~20 years, with the advent of high-growth, high-margin companies, these historical multiples have not really worked reliably to value and compare companies.

Below is a new methodology — the PCG multiple — as a more useful metric.

A Short-ish History of Valuation Multiples

Every asset is only as valuable as its expected return. When comparing companies, investors are considering “how much cash do I believe this company can generate long-term, to reward my investment today”?

This concept is known as long-term Free Cash Flow, and is basically the only thing that matters in predicting a company’s “terminal value”. So, every valuation multiple is simply a way to go “upstream” on the predictors of FCF.

The journey in a financial statement looks roughly something like this:

Assets are invested to produce

→ Revenue

less: Cost of Goods Sold

→ Gross Profit

less: Operating Costs (R&D, S&M, G&A)

→ Operating Profit (EBIT)

less: Interest & Taxes

→ Net Income

less: Capital Expenditures, etc.

→ Free Cash Flow

Assets are used to produce Revenue.

Revenue net of the “cost of goods sold” (e.g., raw material inputs) results in Gross Profit.

Gross Profit net of “overhead/fixed” costs (R&D, sales, HR, office costs) is Operating Income.

Operating Income after deducting taxes, interest, etc., is Net Income.

Net Income after deducting inflows / outflows of capital is Free Cash Flow.

📕 50+ years ago, companies were valued based on P/B (Price / Book).

“Assets of $X → FCF of $Y (and so Price of $Z).”

The Price to Book ratio worked, because for a long time almost every large, important company was a manufacturing concern: CapEx-heavy, localized, and depending on asset utilization and throughput. A company’s value was derived from how it could turn its assets into profit.

It’s a perfectly acceptable way to value something like an industrial goods company or utility company: an enterprise that is slow-growing, stable, and throws off cash (much like a bond or an income-generating rental property).

Then, we saw the rise of business models that relied more on go-to-market rather than production; a global, decentralized supply chain rather than a consolidated one. Assets didn’t matter as much anymore. Did you know that Pabst Blue Ribbon doesn’t make its own beer? And Red Bull doesn’t have any production facilities? Those are extreme examples, but many companies don’t own or direct the facilities that generate most of the “value” that they sell; Apple, for example, outsources glass production to Corning, semiconductor chip production to TSMC, and assembly to Foxconn.

💸 In an environment such as this, companies have come to rely much, much less on owning assets, and hence P/B became less relevant… with more consistent accounting methodology as well, there was a lot more visibility into earnings. So, you could go one step closer and simply compare companies based on their ability generate profits.

“Net Income of $X → FCF of $Y (and so Price of $Z).”

Hence, P/E became popular for several decades. We’ve also seen evolutions on this framework:

EV/EBITDA (for more… creative financial managers)

CAPE (cyclically-adjusted P/E ratio, part of the work for which Robert Shiller won the Nobel Prize) which normalized the P/E ratio for inflation (and hence for market cycles to a large extent)

PEG (Price / Earnings Growth) ratio which projected earnings forward 12 months and used that as the denominator, to normalize for growing companies

💔 But… When looking at S&P 500 P/E ratios over the last 5 years, the mean was 49, the median was 20, and the standard deviation was 620. That's not a typo.

P/E hence broke (often) over the last 20 years, because of companies that were high growth and unprofitable for a long time. Most of these were technology companies, because software business models were inherently “scalable” (i.e., you could 10x or 100x the revenue of the company with minimal additional costs, on an incredibly fast timeframe) in a way that other non-physical business models just weren’t.

Not all of these companies would end up being valuable. But it’s pretty clear that many such companies do become incredible profit-generating enterprises. This has come to a crescendo with “technology” companies taking over the top 4 spots by market cap in the US, all formed within the last ~40 years (Apple, Microsoft, Amazon, Alphabet), accounting for ~20% of the entire market cap of the S&P 500.

The Amazon Case Study

What’s especially deceiving is that it’s hard to tell for a long time that the company would end up being a juggernaut.

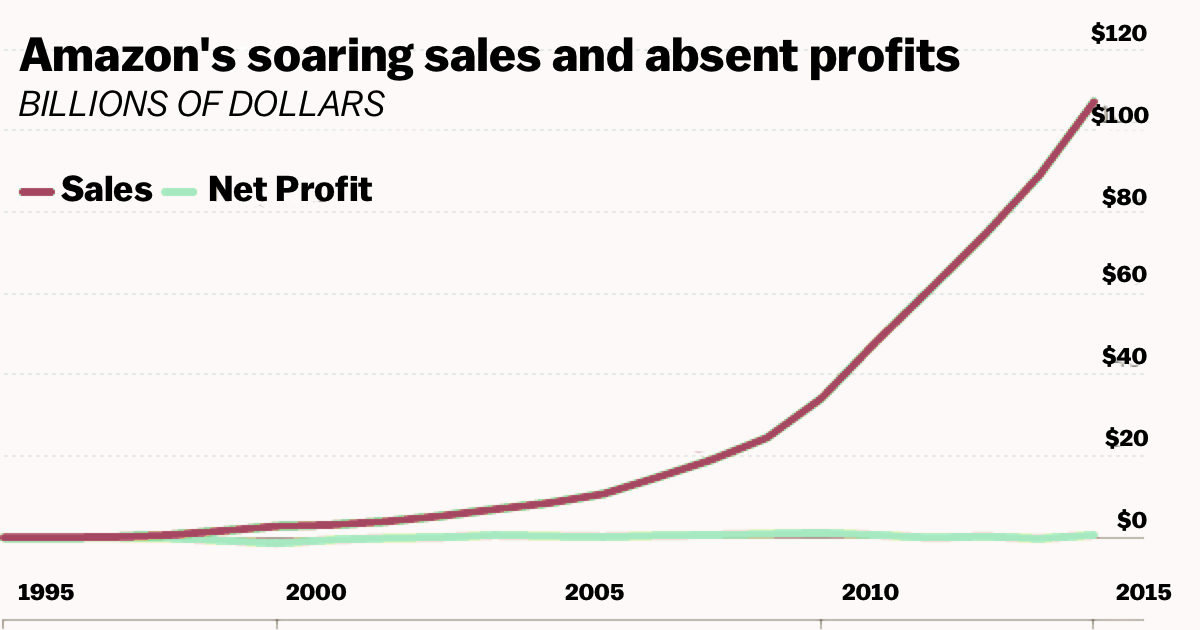

A stark example of this failure of P/E is that Amazon, which — for 20 years after its formation — didn’t really generate any profits, despite massive revenue growth and obviously (in retrospect) strong fundamentals.

Market commentators who focused on profits through 2015 missed the point…

https://www.vox.com/2016/1/31/10873958/amazon-profit-chart

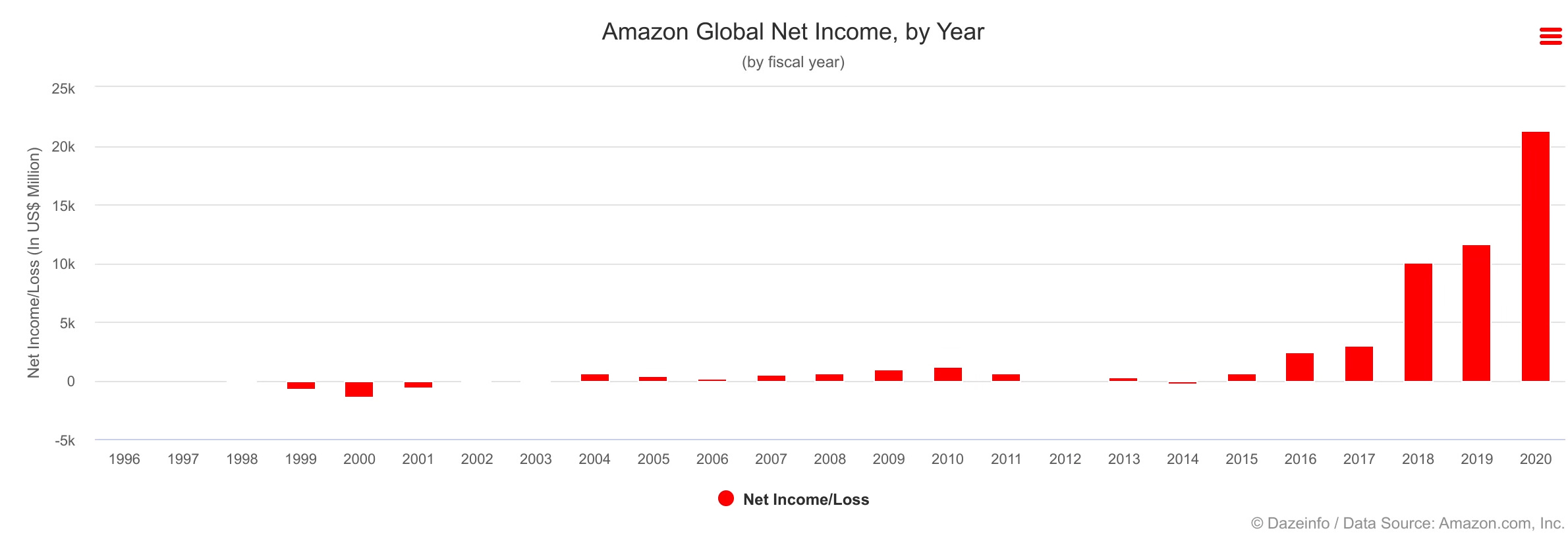

… However, as we’ve all seen, things played out very differently

https://dazeinfo.com/2019/11/06/amazon-net-income-by-year-graphfarm/

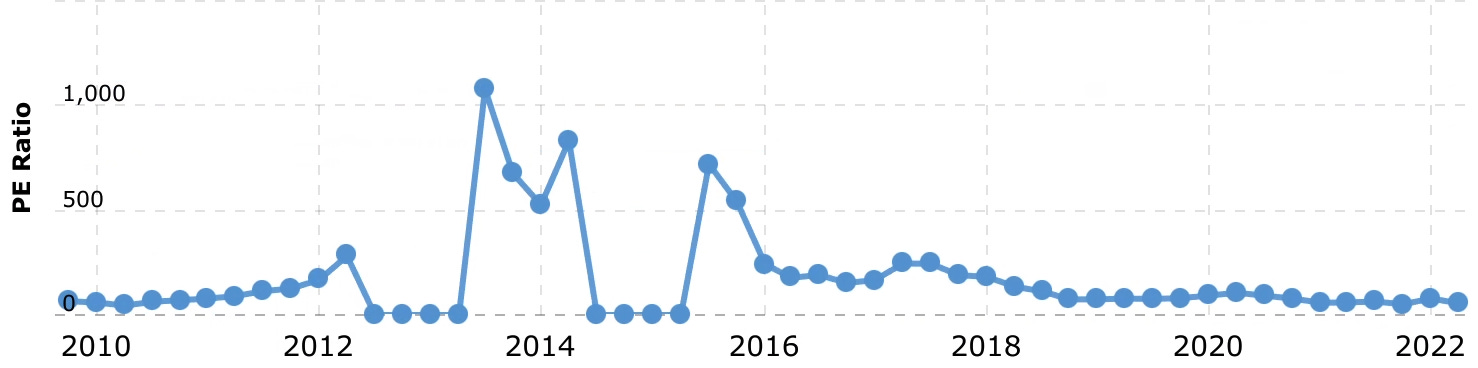

Amazon’s P/E has pretty much never been below 50 over the last 15 years

If it’s that disconnected from the median (20-30x), what’s even the point of using the metric?

Take a look at the scale of the scale of the axis in the graph below! It’s easy to miss. There were also long stretches of nonsensical multiples (200 to 1,000x+); and it just completely broke in 2013 and 2015 when Amazon had brief periods of unprofitability.

https://www.macrotrends.net/stocks/charts/AMZN/amazon/pe-ratio

Importantly, this happened because the exclusive emphasis on current earnings, as represented by P/E. Hence, this metric has completely failed for several decades in Amazon’s history. To quote Ben Graham (can any post on valuations be complete without the godfather 😄):

In the short run, the market is a voting machine but in the long run it is a weighing machine.

30 years is a pretty “long run”. It’s probably not that the market and analysts have been wrong for decades and the ratio has been right… it’s probably the other way around. You could write similar case studies for many, many other companies.

📈 Hence, starting in the 2000s, the frequency and importance of fast-growing companies that were unprofitable (or barely profitable) made P/S (Price / Sales) the multiple of choice.

“Revenue of $X → FCF of $Y (and so Price of $Z).”

But, as you’ll see below, this multiple always had intrinsic issues with it.

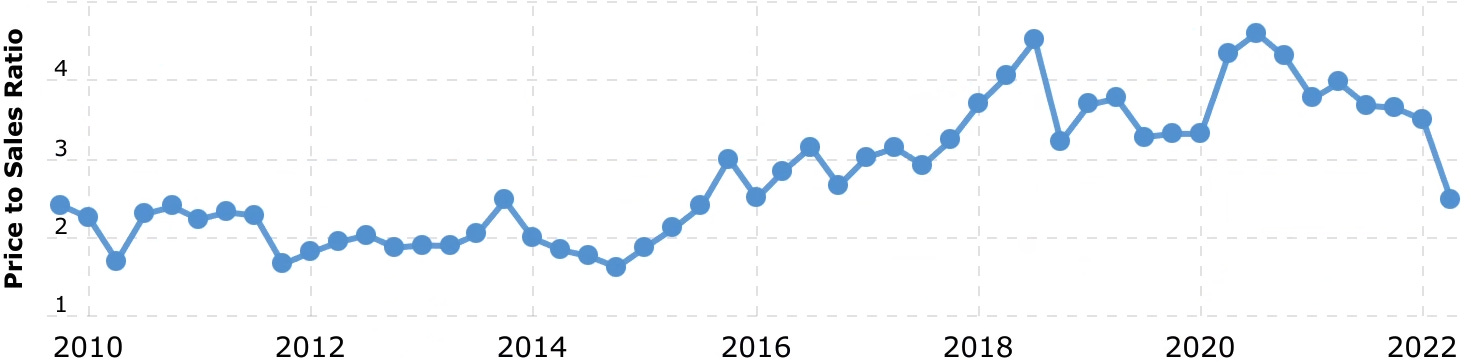

At first glance, P/S solves for this issue! It’s been consistently in the ~2-4x range, which makes it much more reasonable, much less wild.

https://www.macrotrends.net/stocks/charts/AMZN/amazon/price-sales

🏧 So… is P/S is the right way to value companies in this era? Unfortunately not, and it really broke in the last ~10 years, for 3 reasons.

It didn’t solve the issue of signal to noise in multiples, and arguably was worse than P/E when considering the entire market

It didn’t account for growth rate at all, which is one of the biggest contributors to the crazy divergence in P/E ratios we were seeing

It didn’t account for — in fact, it might even have encouraged bad behavior by — a crop of companies that looked like good businesses based on their revenue and growth, but had terrible unit economics and no clear path to profitability… even in a multi-year or decade-long horizon. The ability to generate and grow revenue is a necessary but insufficient condition for a sustainable business foundation (one that leads to long-term cash flows).

A Better Multiple for Valuing Companies

My Experience in Dealing with Valuations

🤷 In other words… why should you care what I think?

During my time in consulting I built many, many DCF models and perused hundreds of financial statements and 10-Ks for (mostly profitable) Fortune 500 companies. Subsequently, I moved to Silicon Valley, and spent a lot of time thinking about valuations for high-growth unprofitable companies. I’ve overseen or directly closed nearly $1 billion in secondary transactions in a range of unicorns, and handled dealflow more than an order of magnitude greater than that (when I was COO at the pre-eminent secondary marketplace, Forge). I also invested in 100+ late-stage and early-stage startups personally.

During that time, the talk of valuations and multiples helped click something into place for me. Because these were all unprofitable companies (pre-IPO unicorns), investors exclusively discussed P/S, but it varied wildly… some public companies (Nutanix, Box, etc.) were trading at 3-4x sales… but many public and private companies were at 50x+. With early stage companies, some of these multiples got even crazier… 100x, 300x revenues, sometimes more!

Reasoning that Gross Profit and Growth are Essential Inputs

This obviously doesn’t seem like a reliable metric, but people were comfortable relying on it all the same. When you asked these (smart) investors and observers “why does company A trade at 10x sales and company B trade at 60x sales?”, the answer fell into one of two buckets:

B is growing so much faster than A!

B has much better unit economics / fundamentals than A!

It struck me as very odd that both of these were quantitative metrics, but somehow were treated as black box, abstract concepts that couldn’t fit into a formula. Instead, they did have mental heuristics which exist for a reason, which would allow you to justify:

two different SaaS companies, A growing at 30% and B growing at 200% being valued at 10x vs. 60x

two different companies of identical growth rate (let’s say 100% growth rate): A in a brutal, 15% margin business, and B being a great business with 90% margins being valued at 10x vs. 60x

😮 Growth Rate and Unit Economics (i.e., Gross Margin) can explain almost all of the variability in P/S.

And when you account for that, you end up with the PCG multiple.

Most importantly, by accounting for these factors, the PCG multiple allows a market observer to compare

- across any industry

- across any stage or growth rate

- across stages in the economic cycle

- with a tight multiple ranging from ~2 to ~12

(rather than calibrating across a range of 10x-1,000x!)

PCG = Price / Compounding Gross Profit

Price = Enterprise Value of the company (i.e., Market Cap - Net Cash on the balance sheet)

Compounding Gross Profit = Gross Profit * (1 + Growth Rate)ᴺ

💡 PCG finally helps us make sense of why a company with $100M in revenue can have a (fair) valuation similar to a company doing $1B in revenue — when you adjust for critical factors like margin profile and growth rate.

Where N varies based on the market environment. This is the equivalent to the adjustment provided by the the Shiller P/E ratio (i.e., this factor acts as a cyclical adjustment).

In a steady state or typical market N = 3.

In an “inflated” valuation market, which are often caused by low interest rates or very friendly monetary policy (e.g., 2020-21), N rises to 4 (or more), which means that companies often trade for well-above "fair" values stated above.

As you can infer from the formula, companies that aren’t growing aren’t very impacted one way or the other, while high-growth companies benefit disproportionately. This is, in fact, what we observe.

In a “tight” valuation market, which are often correlated with recessionary or rising interest rate environments (e.g., mid 2022), N falls dramatically, which means that companies trade lower (and high-growth companies are hurt much worse).

This is why we’ve seen a major haircut in mid-2022 without a material change to a given company’s fundamentals… a change in N from 4 to 2 in a short span causes a company that was doubling every year to drop 75%.

This happened due to a host of macroeconomic factors (Fed hiking interest rates → discount rate increase; geopolitical uncertainty; supply chain issues lead to fulfillment issues).

Add in a headwind of slowing growth rate (software companies benefited from a generational digital transformation in 2020-21 due to COVID, which has quickly faded).

The Actual Multiple Serves as a Proxy for "Quality" of a Company

🗒️ Note: this section was written in 2021, but based on the market cycle at the time. Since the market cycle factor N has changed from 4 to 2, and since then the calculations have not been updated; but valuations have also fallen, so these should hold up relatively well; but some multiples may have shifted from a 6 to a 5, for example.

Most companies trade at a multiple of ~6. For example, Nike, Oracle, Accenture, Google, Microsoft, all trade around here, fairly consistently.

However, they range from 2 to 10, based on the "quality" of the company. Some examples below.

Businesses with low switching costs, highly capital expenditures, or a weak moat often have an M of 4-5. For example, Box, Dropbox, Amazon, T-Mobile, AT&T, Autozone, Costco, IBM, WMT, etc.

Note that this doesn't mean they're a bad company. Everyone would say that Amazon and Costco are incredible companies with a strong moat. However, they do face some structural disadvantages (specifically around how capital intensive they are). But they both have better multiples (~4.5-5) than WMT, which is at ~3.

As you might predict, some companies in here are unexpected. Facebook has consistently traded in the 4-5x P/GG range for years now. It's been probably 6-7 years since it traded at 6-8. Is this because of public perception and/or regulatory scrutiny in recent years? Hard to say.

Businesses with strong moats, network effects, negative net churn, etc. often trade at an M of 8 or sometimes even 10. For example, 3M, Apple, Coca-Cola, etc.

Unsurprisingly, these happen to overlap heavily with the kinds of businesses Warren Buffett likes. Interestingly Apple traded at ~7-8x P/GG multiples in 2016, then dipped and stayed at 5.5-6 between late 2016 and mid 2018, which was exactly Berkshire's buying window. In recent years it's been at 9-12, and he's been trimming his stake.

And again, some businesses show up in this category when I didn’t expected it. Adobe, ADP, and Waste Management, for example, trade at ~8-10. Sure, they're sticky business models, but is Adobe stickier than Oracle, for example? I'm not sure.

Places where the PCG approach breaks

Hypergrowth companies. If a company is quadrupling year on year, squaring or cubing it (or more!) naturally results in absurd numbers (a 500x+ gross profit multiple).

This is of course a challenge with any exponential function; at an extreme, it goes asymptotic.

One workaround that appears to work is to cap the (1+Growth)^N value; it’s a clumsy but workable solution.

The Valuation Calculator accounts for this cap.

Fact of the matter is, companies that are growing at an insane pace are simply hard to value.

Companies with dramatic fluctuations in gross profit. Tesla drives the model absolutely crazy, and so did Boeing during its rocky 737MAX recalls.

Financial services companies. Gross Profit is often hard to calculate for these companies (indeed, it is often not even reported on financial statements), so other multiples such as P/E might still be the right way to evaluate them. Using revenue as a proxy for GP works sometimes but not always, in a pinch.

Why Gross Profit? Where PCG fits in when analyzing financial statements.

When assets were a reliable predictor of long-term cashflows, P/B made sense. It was an imprecise predictor, but investing methodologies were still rudimentary, and it was good enough for that era.

Assets → Revenue → Gross Profit → Operating Income → Net Income → Free Cash Flow

When companies proved you could generate value and profits in asset-light models, and investing became more sophisticated with things like DCF models, P/E became the go-to; investors ignored the antecedents of Assets & Revenue, and focused on Profits.

Assets → Revenue → Gross Profit → Operating Income →Net Income → Free Cash Flow

However, when it became clear that some companies reinvested profits, or built foundations for a long time based on strong fundamentals, then only looking at current profits seemed short-sighted… not long-enough horizon, and ignoring critical inputs. So we pulled back a bit.

Assets →Revenue → Gross Profit → Operating Income → Net Income → Free Cash Flow

And now we find ourselves in a situation where Revenue is a fuzzy, imprecise predictor, because Revenue often but not always leads to Profits; is still very high standard deviation; and all of these multiples ignore growth rates. So where to from here? Given that the underlying logic of this “value chain” still holds, the secret to effectively value companies still sits somewhere in there.

As discussed above, P&L typically breaks down into:

Assets are invested to produce

→ Revenue

less: Cost of Goods Sold

→ Gross Profit

less: Operating Costs (R&D, S&M, G&A)

→ Operating Profit (EBIT)

less: Interest & Taxes

→ Net Income

less: Capital Expenditures, etc.

→ Free Cash Flow

Let’s start over and figure out which metric is the most “predictive” or critical from a first principles perspective.

We’ve already established why P/B and Asset-based evaluations don’t work; and why Revenue alone is a bad indicator of future success, because it doesn’t account for unit economics, and the signal to noise is no better.

Assets are invested to produce

→ Revenue

less: Cost of Goods Sold

→ Gross Profit

less: Operating Costs (R&D, S&M, G&A)

→ Operating Profit (EBIT)

less: Interest & Taxes

→ Net Income

less: Capital Expenditures, etc.

→ Free Cash Flow

While EV/FCF is really the only metric that matters (”in how many years will I get paid back for purchasing this share of stock?”), it really only applies for thoroughly mature companies which operate “like a bond”, and whose CapEx are either fixed (i.e., maintenance mode or zero). Really, what we’re trying to predict here is (Future EV) / (Future FCF), and in a weird way, higher CapEx can lead to future FCF, so lower FCF could be — in some cases, like Amazon — inversely correlated with Future EV.

To put it differently, EV/FCF doesn’t work well for any company that is trying to grow or invest (which every company aspires to). So let’s rule out FCF as the “key metric.”

Interest & Taxes are either a) exogenous or b) a function of the company’s financing structure (debt vs. equity), but not necessarily a predictor of the quality of a company’s business in the long term. This is also part of the reason why P/E isn’t always sufficiently predictive. So let’s rule out Net Income as the “key metric.”

Assets are invested to produce

→ Revenue

less: Cost of Goods Sold

→ Gross Profit

less: Operating Costs (R&D, S&M, G&A)

→ Operating Profit (EBIT)

less: Interest & Taxes

→ Net Incomeless: Capital Expenditures, etc.

→ Free Cash Flow

So that leaves Operating Profit and Gross Profit.

If you’ve ever run a DCF model for a company over a 5-10+ year horizon, there’s a fun fact you’ll recognize right away… the difference between the two, which is operating costs (R&D, S&M, G&A) are always a “plug”. They’re always a placeholder value that isn’t quite flat but of course doesn’t scale linearly with revenue. So… it’s always a made up value.

So if you’re really trying to estimate long-term-anything, why on earth should that be a major determining factor?

Those are also — if invested in correctly — the departments that “scale well.” 10xing your revenue shouldn’t require 10xing your HQ staff (that’s why it’s a plug in DCF models, after all). If you trust a company’s execs to build their organizations well, your operating costs pay off in the 2-5+ year horizon via better innovation, or brand, or operating efficiency.

On the flip side… I know from personal experience that optimizing for EBIT and cutting HQ headcount (which happens all too often at stagnating companies in the interest of “shareholder value”) is the wrong strategy almost every time. It leads to underinvestment in engineering, or loss of brand value and go-to-market strength, it skinnies out your HR team which leads to crappier employee experiences or bad recruiting, and so on.

So… that means that the only predictor of a company’s long-term free cash flow is not:

companies that spend on operating costs; that can pay off if done well

companies that spend on interest (it’s a function of capital structure) or taxes (exogenous)

companies that spend on CapEx; that can also pay off if done well

It is, in fact, a function of:

companies that have strong unit economics

Which leaves: Gross Profit as the critical metric.

If you take a step back, this relatively quick calculation (growth rate ^N * gross profit) approximates the recommendations of a full-fledged DCF model; because it gives weight to critical inputs (gross profit and growth rate) and ignores the variables that end up being “plugs,” anyway (operating line items).

No multiple or metric is perfect, but this is why this approach produces a **much ** lower error bar than other typical metrics such as P/E, P/S, etc. This produces a Back of the Envelope Discounted Cash Flow Model, if you will. BOEDCFM doesn’t quite roll off the tongue, though, does it? So let’s stick with PCG 😆.

Other Thoughts on the Benefits of PCG

You’re suddenly able to compare a brick-and-mortar retailer to a high-margin software company – something that has never been possible before.

Gross Profit accounts for the fundamentals of a company (specifically, in ensuring that their business model / unit economics are healthy).

If accounting is competent, it factors in the cost of “buying revenue”, through promotions, discounts, or other artificial efforts to boost revenue. This was already becoming a factor because of companies in the mid-2010s to “blitzscale” by buying revenue.

When you look at the P&L of a company that hasn’t fully matured yet, Gross Profit is probably the best predictor of profitability when they are at scale. The rest of the line items "scale better" (i.e., fall as a percent of sales as a company grows: Sales & Marketing; General & Administrative; Research & Development).

Note: particularly for companies with cyclical revenue (e.g., retail), using LTM (Last 12 Months) gross profit is necessary, instead of annualizing quarterly gross profit.

Variances in the quality of a given business — ability to innovate, brand power, stickiness, operating efficiency, etc. — cannot be folded into the input metrics or existing profit, because those are early investments which take years (sometimes decades) to pay off. Instead, they are usually expressed in the final multiple itself.

This “X-factor” — why does a company trade at 3x vs. 7x is the final frontier for the judgment of an Intelligent Investor.

No multiple is meant to solve for that "X-factor"; rather, its role is in enabling an investor to normalize valuations across companies so that they can make educated decisions on whether and where to deploy capital.

By accounting for all the other numerical factors, we leave it to the judgment of an investor whether a company has strong or weak fundamentals, as measured by the stickiness of their business model, their capital intensivity, their corporate culture and ability to execute, their brand and IP moat, and so on.